Blog

Industry Insights, Press Release

Industry Insights, Tech & Visibility • Published on June 5, 2023

The future of trucking is neither traditional brokers nor asset carriers; it is a new model, which we will call the hybrid carrier.

This model gets materially better with scale, using technology to address the industry’s existing limitations and the reasons that trucking remains so fragmented. Hybrid carriers have a digital truckload marketplace, a universal pool of trailers, online drivers and equipment, and broad industry integrations, all running on a technology platform that uses data and AI to orchestrate everything, manage carrier quality, and generate actionable insights for shippers. By removing silos around truck and trailer capacity, these truckload platforms will benefit from network effects and other economies of scale, making them better and cheaper at scale and giving shippers compelling reasons to consolidate their freight spend for the first time.

At the end of the day, there is a reason that trucking is so fragmented and hasn’t seen benefits of scale. Here we dive into why this is and why it is now changing.

In most transportation and delivery businesses, economies of scale, including network effects(1), allow the leading providers to gain cost and service advantages for their customers, causing the market to consolidate around them. The parcel and less-than-truckload (LTL) delivery businesses are good examples of this. No single package takes up an entire truck or trailer, so each customer that ships something helps cover the cost of the delivery for everyone. The more participants, the more economical it becomes. Additionally, with more customers and packages, the shipping service can add more deliveries per day, making it even more convenient for everyone.

This has not yet happened in the truckload industry(2), where limited advantages of scale have allowed fragmentation to persist as a viable sourcing strategy. Shippers work with dozens or even hundreds of truckload carriers and brokers who compete for their business. This is currently the best strategy for shippers to get competitive coverage, pricing, and service, but it leads to a transitory or what-have-you-done-for-me-lately mentality that limits the opportunity for each individual provider to think long-term, and it prevents big bets that could lead to step-function improvements in service and cost. For this to happen, shippers need to be presented with a fundamentally new model.

This persistent fragmentation in truckload is unusual. Most of the time, when companies source services, they choose just one or a few providers, not dozens or hundreds. They want to reduce the overhead of managing vendors and gain the volume discounts and priority service of top customers. For example, companies pick one payroll processing system, hire one partner for warehouse logistics, and contract one food services vendor to manage their cafeterias. The leaders gain advantages as they get bigger and customer growth accelerates.

Metcalf’s law says that a network’s value is proportional to the square of the number of participants (n^2); said differently, its value increases exponentially as its users or participants grow. These models clearly benefit from this effect. Why not truckload?

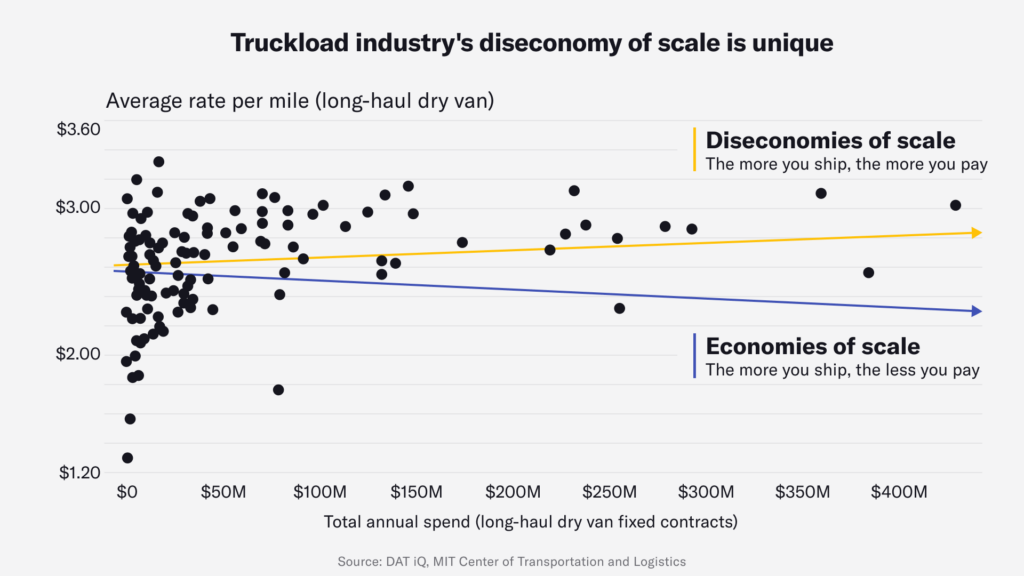

Unlike in the parcel or LTL examples, each truckload delivery is financially viable on a standalone basis. Its cargo fills the entire truck on its own, and it moves point-to-point along a single route, so its success does not rely on any other participants in the network. For this reason, the barriers to entry are also very low. Nearly anyone can buy a truck or fleet and start hauling freight on similar footing to the rest of the industry.

Therefore, the network effects in truckload come not from optimization at the individual truckload shipment level but rather primarily at the system level. In parcel, wasted “space” creates the primary inefficiency to solve. In truckload, it is wasted miles (driving empty) and wasted time (waiting to load/unload) that creates the primary inefficiencies to solve. For example, combining multiple shippers’ freight networks to identify the best combinations of loads (routes, backhauls), optimizing appointment times and drop-and-hook programs to reduce waiting time, and ensuring that the best-located truck is matched to each run to reduce empty miles.

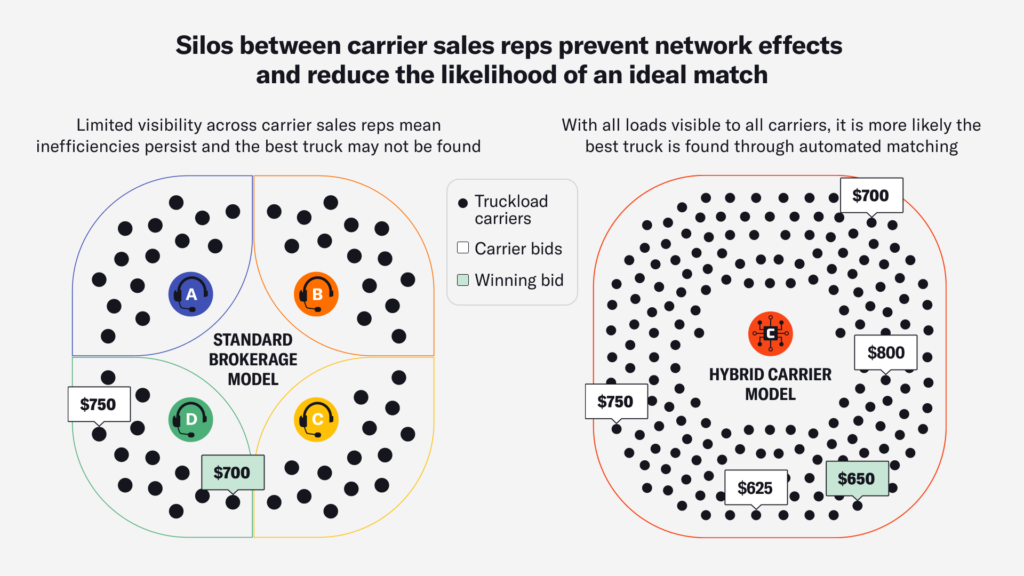

Unfortunately, many of these truckload networks are walled off from each other today. For example, the business model of the market makers who are in the best position to orchestrate the industry today – large truckload brokers – often operate on a load-by-load basis and fragment their own network of trucks and shipments into many small marketplaces, each managed by a carrier sales rep with a portfolio of carrier relationships. Naturally, carrier reps are reluctant to share their trucking relationships with others, which blocks a true network from forming as the brokerage scales.

On the other hand, asset-based carriers run businesses predicated on effective network planning, which shouldn’t come as a surprise. While a typical broker is “asset light” — their primary cost being wages to employees who earn a commission for sourcing loads from shippers and finding trucks to do them at a lower cost — an asset carrier’s primary costs are their assets (trucks and trailers) and fixed driver costs. Not only do they need to be smart about making enough money to cover their variable costs, but also to cover their cost of capital for the assets they own. Thus, their focus is on asset utilization. They consider how different shippers’ networks overlap, and they attempt to stitch together a balanced portfolio that maximizes the utilization of their assets. For example, in an ideal situation, a carrier would find a backhaul or other symmetrical route between two companies that ship in different directions, creating an efficient loop for their drivers. In another case, they might start with a pool of trailers at one facility that ships to several destinations and, over time, fill in backhaul contracts to recover the empty returns.

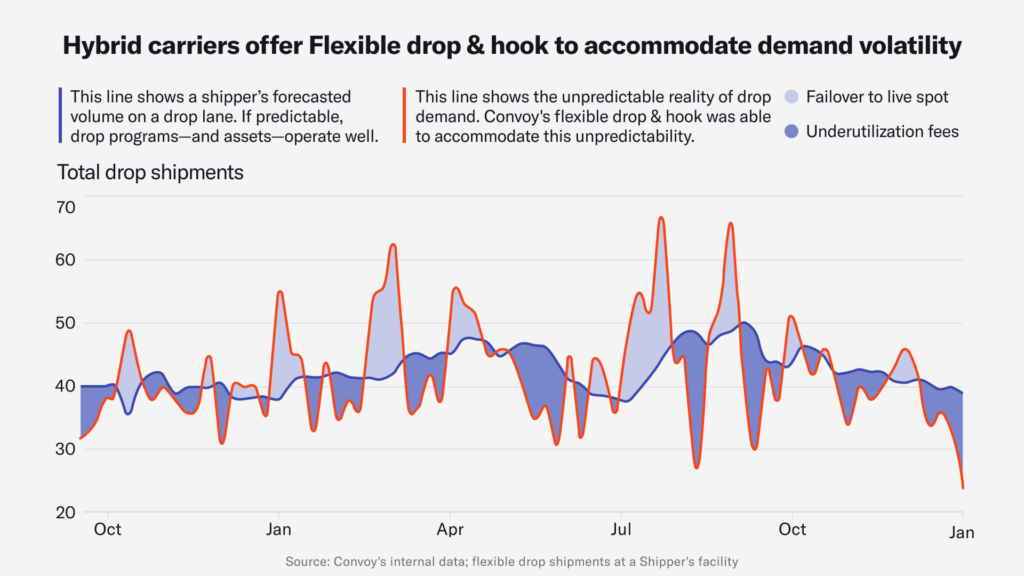

However, as things move from planning to execution, it becomes clear that forecasting is often more art than science. Trucking is messy; the allocated pool of trailers and dedicated drivers are more fixed than daily or weekly fluctuations in demand, the necessary appointment times for live-load scenarios aren’t always available, and facilities, trucks, and drivers get delayed. And if something goes wrong, changing the appointments and driver schedules is cumbersome. The asset model is rigid by design, making it hard to be resilient when the unpredictable inevitably happens. Holiday weeks are a typical example of this. For example, leading up to Labor Day weekend, load volume spikes and outstrips trailers, leaving shippers to fail over to find the live-loaded trucks on the spot market. During off weeks, when volume dips, they pay trailer underutilization fees.

Adding or removing trailers quickly is expensive and operationally difficult. Trailers are committed, and the drivers have a system. Thus carriers manage a constant tension between service levels to shippers on the one hand and asset utilization on the other hand. And even though most asset carriers also run a traditional truckload brokerage to gain flexibility – re-brokering up to 40% of their freight to other carriers (3) – it is not seamless with their own operations, and its costs and service levels often don’t hold up to the commitments they’ve made.

All of these dynamics reduce service flexibility and lead to local optimizations and sub-scale marketplaces that lack network effects.

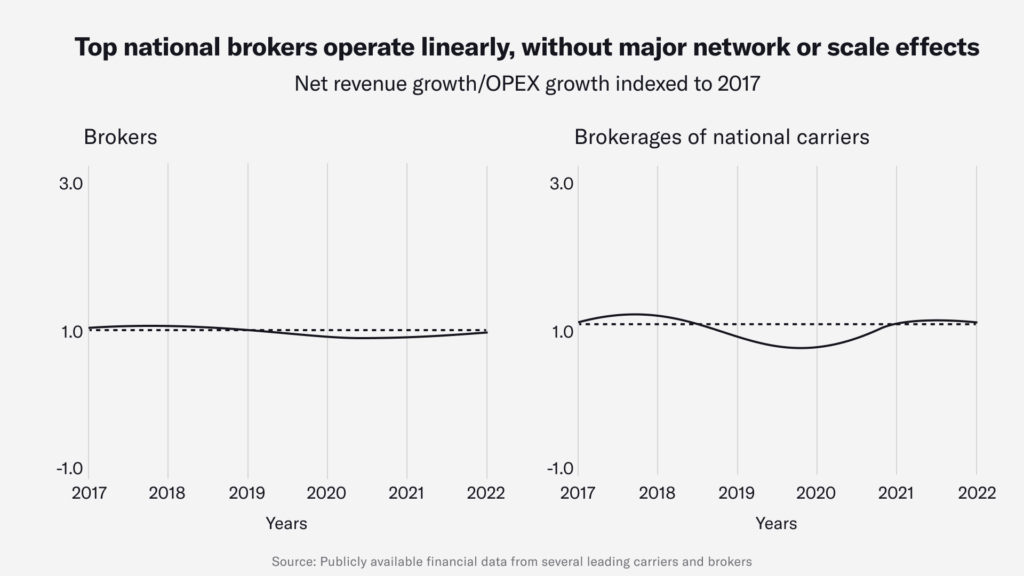

For example, you can see below that for several top national brokers, every incremental $ of net revenue requires proportionally the same investment of additional operating expenses. In other words, these businesses operate linearly, without major network or scale effects.

This doesn’t change as brokerages or carriers get bigger. In 2018 I listened to a panel discussion on trucking at a conference. A new-to-truckload executive shared that after looking at the financials of over a dozen public and private brokers, he had a discovery to share — all of them, from sub $100M to several billion in revenue, had roughly the same unit economics. The large, national players could cover the largest shippers across more regions, but they didn’t do it better. Others in the room echoed this for asset carriers, and others shared that in some cases, they became slightly worse with scale because their overhead increased, and they struggle to maintain the same quality standards, pricing controls, and network balance.

It isn’t that brokers and carriers don’t get better as they learn a facility’s operations or build density on a lane. They do. However, the financial improvements are localized to that specific opportunity and quickly reach a plateau. Similarly, those that add offices and employees to gain national scale are able to service larger national accounts, but as they grow, each incremental shipment costs about the same to support.

Finally, in most cases, shippers need multiple providers to meet their needs. Some of their freight is predictable and runs drop & hook, best for asset carriers, and some is less predictable and benefits from a broker’s flexible capacity. For national shippers, there isn’t one carrier or broker that is “best” in all regions of the country. And at the end of the day, because they can’t precisely forecast their volumes unless they pay for fully-dedicated capacity, shippers can’t count on their carrier or broker partners to reserve capacity for all scenarios. They simply need redundancy, opening the door to many providers.

All of the above conditions across asset carriers, brokers, and shippers’ truckload networks have created antibodies to consolidation. The Vice President of a major national U.S. retailer summarized this to me by saying, “We have hard caps built into our system. I can tell you that whenever we relax this and give a huge award to one carrier, even a carrier-of-the-year winner, it backfires, and their service drops the next year, and we move them back out.”

To date, a model that gets more efficient and better for shippers as it scales has not existed. As such, the conditions for significant industry consolidation and simplification have not existed previously, but that is now changing.

A hybrid carrier brings together the best of asset carriers and truckload brokerages, using technology and open capacity marketplaces and shared trailers to get better and cheaper with scale in a way that we have not seen in the truckload industry. Over the next decade, a handful of hybrid carrier-enabling platforms will emerge and scale as they power this transition, giving today’s brokers and carriers the opportunity to deliver a broader set of service offerings with higher performance, better cost structure, and more data-driven insights for their customers.

The key ingredients of a hybrid carrier include:

The shared trailer pool is not tied to a given facility or route, so it can quickly grow or shrink with weekly volume changes faster than traditional carriers. This allows backup and spot loads to run as drop & hook as well. Any carrier on the platform can move a pre-loaded trailer, rent an empty one, or keep it after a delivery to use for other off-network jobs before later returning it. The return locations and times are designed to get trailers to where they are most needed on the network (or predicted to be needed by AI). This flexible return and rental program reduces relocation costs and allows carriers to find more backhauls. The platform maintains the pool.

Hybrid carriers have access to vast pools of carriers and owner-operators. To drive network effects, they need to know that their path to getting access to the best freight at the best rates is via the digital marketplace, not negotiating over the phone. If their ideal job is out there, they can get it. This brings energy to the marketplace, which includes single jobs, batches, dedicated runs, and more. The variety of options allows for a trade-off between performance and cost. This results in asset-like visibility, availability, and performance, even with minimal lead time.

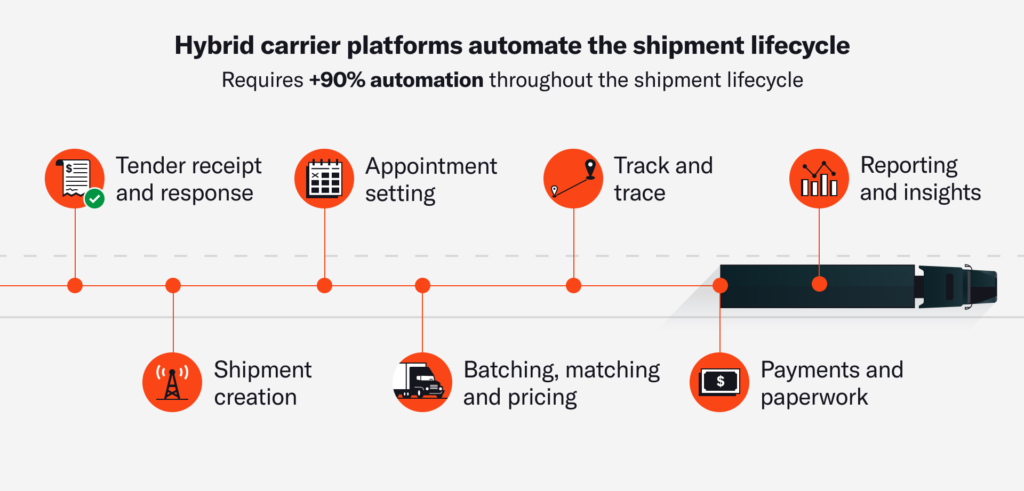

It isn’t enough to have some of your carriers/drivers do some of their tasks online. To give the hybrid carrier the greatest opportunity to harness efficiencies and find opportunities, all drivers and trucks need to be online, when on the clock, for all the steps. Drivers share data and documents, offer visibility, handle detention and accessorials, manage payments, self-service exception handling, and more. The tech helps drivers keep moving to make more money and get paid faster. The visibility helps the platform learn and become more efficient. Today, the trucking companies most likely to use the app have < 10 trucks.

Hybrid carriers have digital connectivity into a broad range of shippers via TMS and other EDI or API integrations. These allow for automated tendering, routing guide updates, spot load bidding, appointment scheduling, and financial processing.

A hybrid carrier is too complex to run only by hand. The platform orchestrates the pricing and matching, provides self-service tools for brokers and carriers, tracks and manages carrier compliance, monitors and repositions trailers, and supports workflows for tendering, load creation, appointments, visibility tracking, payments, insights, sustainability reporting and accounting (e.g., GLEC framework).

Over the last decade, billions of venture dollars have gone into the truckload freight industry on the promise of digital transformation. That investment spurred, amongst other important innovations, the first generation of universal trailer pools and digital platforms for truckload brokerage, including many of the capabilities listed above. These platforms have remained proprietary, but this is changing. In the coming years, we will see some or all of these platforms open up, and the next wave of innovation will be built on top of them, enabling today’s brokers and carriers to become tomorrow’s hybrid carriers too.

As this happens, the leading platforms will only get better, leading to increasingly better cost, service, and insights for shippers. For the first time, shippers will have a compelling reason to consolidate their freight onto fewer providers.

The proof, as they say, is in the pudding. While it will take years to know exactly how this plays out, Convoy is one of the companies that has invested in building a hybrid carrier platform already. The results that we have seen from our V1 are very promising, and here are a few examples.

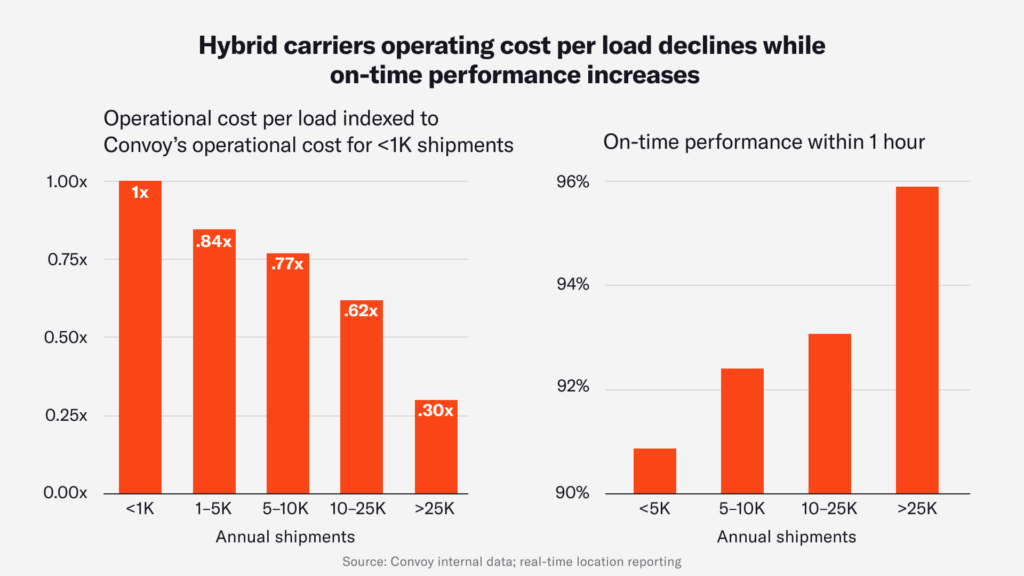

There are material operating cost advantages when shippers consolidate more of their freight onto one hybrid carrier. The example below shows this for Convoy’s current offering, which is powered by our hybrid carrier platform. In addition to cost reduction, we also see improvements in on-time service performance.

As the volume of loads and trucks in a market grows, network density increases, and the odds that a carrier finds their ideal load(s) (ideal timing and route) increase, reducing waste and costs. This phenomenon isn’t new; however, in most cases, brokers see the gains tap out and plateau relatively quickly. Instead, Convoy sees the gains come in waves with each efficiency, including overall density, load batching, appointment time optimization, flexible trailers, etc. The system continues to improve as it scales.

Hybrid carriers enable flexible drop & hook, which we have observed to successfully handle rapid changes in freight demand without needing to failover to live spot or paying underutilization fees.

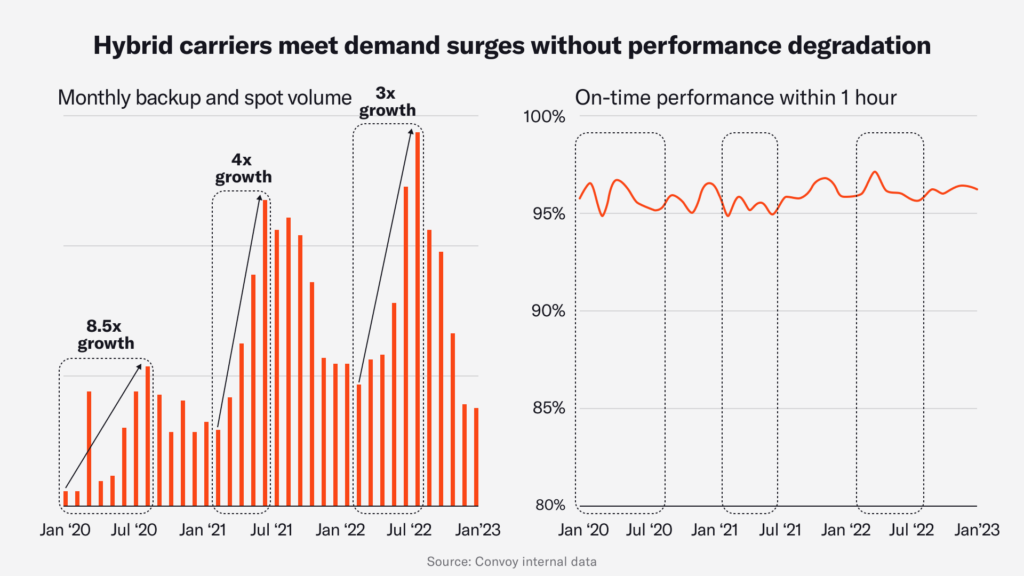

Hybrid carriers can handle volume spikes with minimal impact on service quality because of the scale and automation of the marketplace.

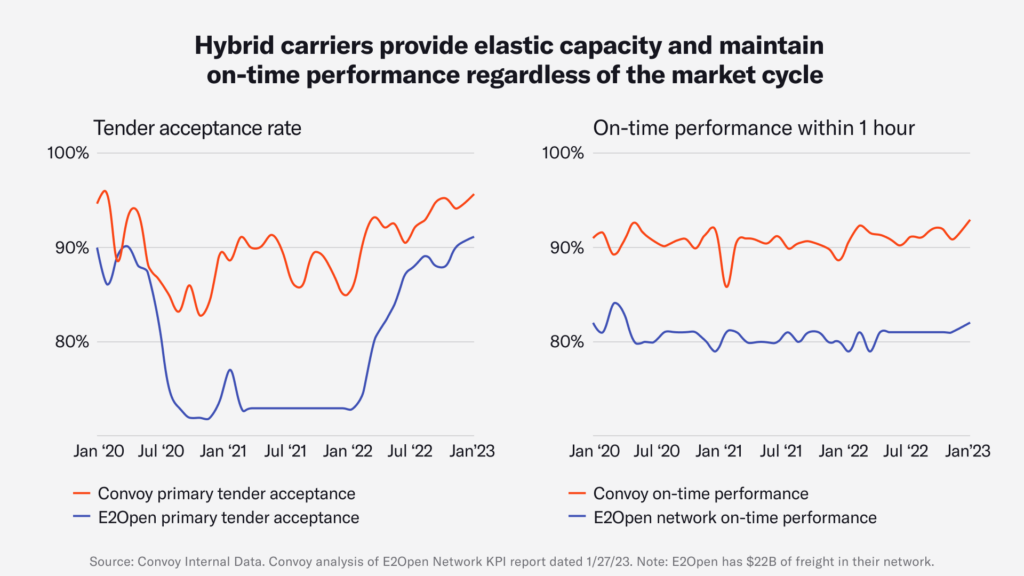

This pattern was maintained through the volatility of COVID. The efficiency of a hybrid carrier-style network provided elastic capacity with high tender acceptance rates and helped maintain superior on-time performance relative to the industry across market cycles.

The truckload industry has long been held back from enjoying the efficiencies and service benefits that come from economies of scale…but that is changing and changing fast. After proving to ourselves, our shippers, and our carrier network that there is a new way to manage truckload that DOES, in fact, get better with scale, we have begun to open up our platform to the broader industry.

Our goal in doing this is to accelerate the trucking industry’s transformation towards a more efficient future. That is only possible by breaking down the walls that exist across the industry. These walls that exist within and across shippers, within and across brokers, and amongst carriers’ assets are impeding the tremendous benefits that can come from network effects and other economies of scale within any single broker and across the entire industry.

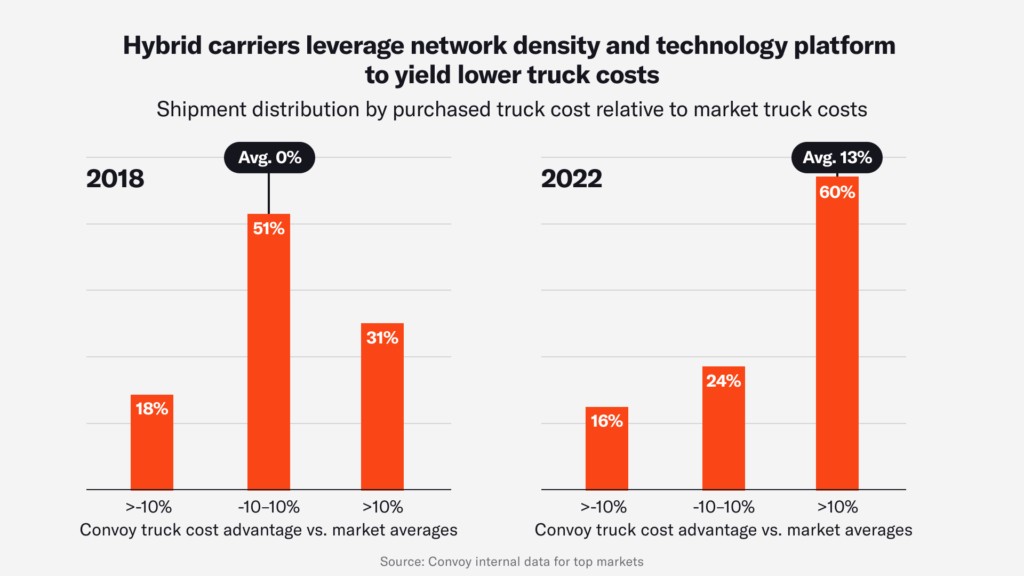

Fortunately, the walls are already starting to come down. Within Convoy, our marketplace for truckload carrier capacity is unfettered by individuals’ various books-of-business, and our trailers operate in a universal pool across facilities and carriers. We recently opened this platform up for other carriers and brokers to use as well, alongside our first party truckload business. The nearly 20 brokers and carriers that are using it today save an average of 15% when they find a more efficient truck on our platform than on their own. And as we release more features and capabilities into this externalized, standalone platform, it will only get better, and momentum will only build further.

As the now famous quote, most often attributed to William Gibson, goes, “The future is already here. It’s just not evenly distributed.” Never before has that been more true than it is today in the US trucking industry.

To learn more, inquire at info@hybridcarriers.com.