Blog

Data Science, Freight Research, Industry Insights

Freight Research • Published on June 16, 2020

Retail sales and industrial production data published this morning by the Census Bureau and the Federal Reserve Board paint the portrait of an economy on the mend. The data showed a rebound from April — hardly a feat given that month’s historic lows — though not quite as sanguine a portrait as employment data published earlier this month. As April turned to May, the economy shifted from the adrenaline rush of crisis management to the slow, halting process of restructuring.

Retail sales data showed there was some pent-up consumer energy unleashed in May: Automotive, clothing and furniture sales all posted double- (or triple-) digit monthly percent gains, but sales remained well below their year-earlier levels. Spending was sharply stronger than production. Factory output increased, but only barely — failing to recover (yet) much of the March or April declines. Capacity utilization held about 10-15 percentage points below where it would otherwise be.

Freight data for late May and the first half of June suggest a strong restart as states reopen, but also a quick fizzle. There is clearly some degree of pent-up consumer demand, but also the enormous weight of economic restructuring, popular anxiety and shifting priorities. The market narrative has swung over the past few weeks from wildly bearish to wildly bullish. Neither quite feels right.

Americans are clearly tired of being cooped up and want to get back to living their lives; many are catching up on purchases they delayed during the shelter-in-place orders. But they’re not quite rushing to return to their former patterns either. Personal services ranging from barbers to bars to doctors are going to have lower productivity for the foreseeable future, and will pass along some of those costs to their customers; factories have more options to adapt — through extended shifts, distributed production, and automation — but will also see diminished capacity utilization; workers left adrift by bankrupt businesses that decided there is no viable path forward will slowly find their way into new jobs, though older Americans on the cusp of retirement may decide that one more round of interviews simply isn’t worth it.

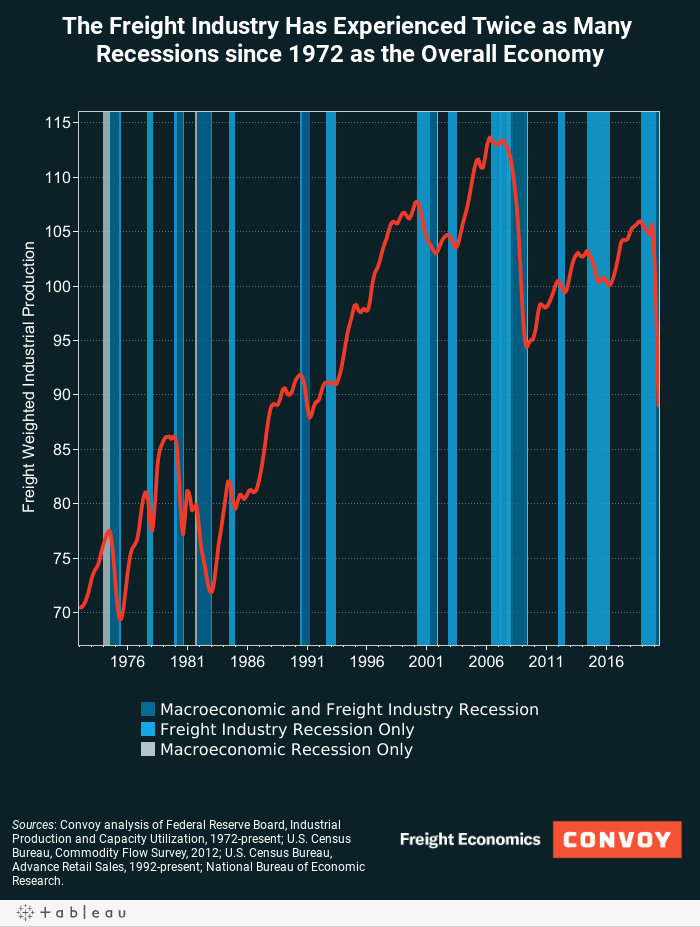

Freight volumes picked up in May, though due caution is necessary when interpreting industry data. Across Convoy’s network, truckload demand from general merchandise retailers surged before slumping during the first half of June (almost like a mini-March), demand from food and beverage manufacturers has been lackluster after record-breaking months in March and April, and demand from industrial manufacturers is inching higher. Despite that, the freight economy remained deep in the year-and-a-half long recession that began in late 2018.

It’s dangerous to read too much into the most recent data point when thinking about how the path ahead. The naive approach is to extrapolate directly from recent developments; that’s almost certainly not how things will play out. The incoming data are going to be noisy because the economy is noisy: Businesses and people are grasping at straws, trying to figure out which way the economic winds are blowing. Consumer spending, factory output, and truckload demand are going to be lumpier — prone to sudden spikes and unforeseen dips.

At times like this, it’s common to hear the sweeping generalization that the freight industry leads the economy. Intuitively this makes sense; in practice it’s not entirely true. As the quote popularly attributed to baseball legend Yogi Berra says: “In theory there is no difference between theory and practice; in practice, there is.”

In “normal” times, there’s a plausible explanation why freight would “lead the economy”: Manufacturers and retailers form expectations about demand for their products far enough ahead to be ready for when consumers want them. Some individual firms are better at this than others, but in aggregate, it provides a window onto future expectations from the forecasters who are likely to know best and, to some degree, play a role in shaping that future.

(This lead time can be anywhere from several months to several days, depending on the industry. The economy-wide shift toward just-in-time production and retailing in recent decades, has eroded the predictive lead of freight data. Practical advantages in predicting economic activity from freight data have more to do with its timeliness of data availability rather than a meaningful structural lead.)

But those producer expectations are vulnerable to surprises (or, “shocks” in economist-speak) just like the rest of the economy. When these shocks hit, when the economy is approaching a turning point, or when there is elevated uncertainty — as there is now — freight follows the economy because the producers and business planners are just as lost as everyone else.

View our economic commentary disclaimer here.