Blog

Industry Insights, Press Release

Data Science, Freight Research, Industry Insights, Shippers • Published on May 15, 2020

For many U.S. households and businesses, April forced us to think hard about what’s truly “essential”. Factory output and retail sales data reported this morning by the Federal Reserve Board and Census Bureau provide a quantitative window onto those priorities.

It comes as no surprise that April was a brutal month for the U.S. economy — industrial production, factory capacity utilization, and retail sales all posted record contractions. This comes on top of March, which itself saw the biggest monthly decline in factory output since the end of World War II.

We’ve known for some time that April’s data would be rough. Anyone who went to a grocery store last month knew that intuitively. Real-time truckload demand over the course of April showed a deterioration in commerce following the early-March surge, then a steep drop as the economy went on pause, which stabilized at a low level only toward the last week of the month.

Some categories moved sharply; others hardly fell at all (or, in a small number of industries, increased).

On the consumer side, retail sales at online stores jumped 22 percent and grocery spending was up 13% from a year earlier while clothing spending fell by nearly 90% and spending at electronics stores was down by close to 50%. All-in-all, U.S. consumers spent about $130 billion less in April than the pre-COVID-19 trend suggests they would have otherwise, and that was on top of about $50 billion in lost retail spending in March.

On the factory side, output of durable consumer goods — mostly big-ticket items like computers, cars, and washing machines — fell 36% in April from March (down 45% from a year earlier), worse than the worst months of the Great Recession and touching its lowest level since 1992. Motor vehicle and parts output fell by 72% from March (down close to 80% from April 2019); factories in the automotive sector ran at around 15% capacity in April. But output of nondurable consumer goods — mostly essential household items like processed food and cleaning supplies — fell only 5.5% (down 7% from a year earlier).

May is already revealing itself to be the opposite of April, though tentatively so. In Convoy’s network, truckload demand increased modestly the first week and more sharply during the second week of May. It’s still only about 80% of where demand was in February, but it has very clearly turned a corner. Truckload demand from consumer staples shippers in Convoy’s network is now above where it was at the end of February and demand from food and beverage producers is only slightly below. Industrial manufacturing is just beginning to restart, and is still 15%-20% below late-February levels.

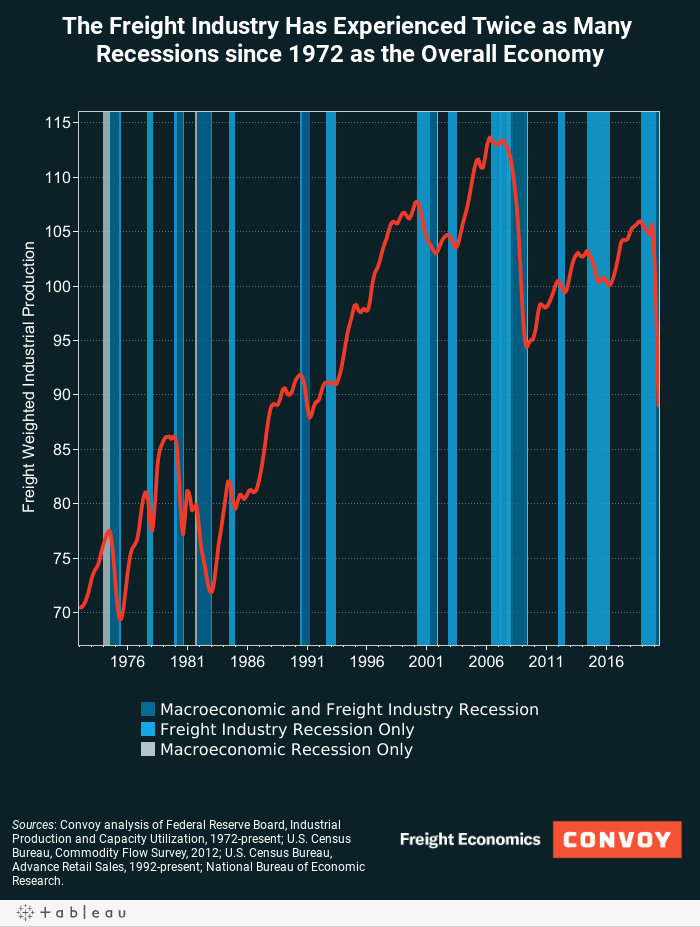

Convoy’s Freight-Weighted Industrial Production index — which weights industrial production and retail sales by their truckload content to provide a snapshot of aggregate truckload demand — fell to its lowest level since January 1994 and remained in recession territory in April, as it has been for over a year and a half now. That is likely to continue for the foreseeable future.

View our economic commentary disclaimer here.